MENU

E+F LEASING

E+F SALES

MENU

-

HOME

-

E+F LEASING

-

E+F SALES

-

-

There was a time when housing stress had a postcode.

If prices surged in one city, you looked elsewhere. If inner-city felt impossible, you widened the circle. If coastal markets overheated, regional towns offered relief. The system wasn’t easy, but it had pressure valves.

That’s what’s changed.

What we’re seeing now isn’t a single market overheating. It’s a broad tightening that stretches from city to country, houses to apartments. And for many people, the result is the same uneasy feeling, that no matter where you look, the numbers don’t quite work anymore.

This isn’t a warning. It’s a reframing. Because understanding why this feels different matters more than pretending it isn’t happening.

The myth of “somewhere cheaper”

For decades, mobility was affordability’s safety net. When one market became unreachable, another picked up the slack.

Today, that safety net is thinner.

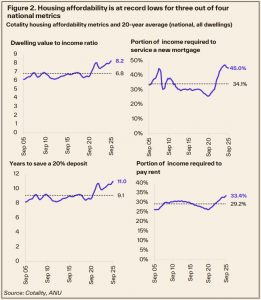

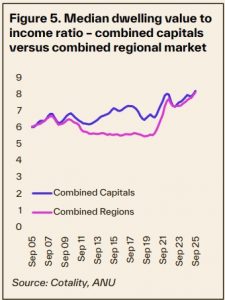

Data across Australia shows affordability weakening almost everywhere at once. Capital cities are stretched, but so are many regional and lifestyle markets that once promised a reset. The price gap between traditionally expensive areas and traditionally affordable ones has narrowed, not because cities became cheaper, but because everything else caught up.

In real terms, this means relocation now often delivers a lifestyle change without the financial relief people expect.

Apartments didn’t escape, they absorbed the pressure

Apartments have long been framed as the rational alternative. Smaller, simpler, more attainable.

And for many buyers, they still are.

But what’s shifted is why unit prices have risen. In many markets, apartments have become the release valve for buyers priced out of houses. Demand didn’t disappear, it redirected. As a result, unit affordability has tightened alongside houses, particularly in well-located, amenity-rich areas.

This matters because it quietly changes the property ladder. What used to be a stepping stone increasingly feels like the final rung.

Prices moved faster than pay packets

At the centre of the tension is a simple imbalance.

Property values have moved decisively upward. Incomes have not matched that pace.

When interest rates rise, that gap becomes more visible. Borrowing power shrinks while prices stay firm. Even buyers with solid savings and stable jobs find themselves constrained, not by desire, but by serviceability.

This is why the housing conversation feels heavier than it used to. It’s less about aspiration, more about arithmetic.

Why this phase feels unfamiliar

Housing cycles aren’t new, but this one has a different texture.

Previous booms were often contained, a city here, a sector there. This shift has been broad and reinforced by structural forces, population growth, limited supply, planning constraints, and the rising cost of construction.

When affordability erodes everywhere at once, behaviour changes. Buyers pause. Expectations soften. Family assistance becomes more common. Renting stretches longer into adulthood. Investors become more selective.

None of this signals collapse. It signals adaptation.

Reading the moment clearly

If the market feels confusing or quietly discouraging, that response is rational. The data supports it.

What matters now isn’t chasing yesterday’s assumptions, but understanding today’s conditions. This is a market shaped less by speculation and more by structure.

At Ethel + Florence, we believe clarity is the most useful starting point. Not urgency. Not fear. Just a grounded reading of where things actually sit.

Because when you understand the landscape, even a tighter one, you make better decisions within it.

This piece reflects publicly available Australian housing affordability data and broader market analysis as at early 2026.

Jul 9, 2026

For nearly two years, the property story in this country only pointed one way. Up. The June figures are the first clear sign that has changed, and it is worth being straight with you about it, especia

Jul 7, 2026

Take a walk through Newstead, South Brisbane or the fringes of the Valley and count the cranes. It is easy to assume new apartments simply appear, or that somewhere a government is building them. Neit